Grokking Retirement Accounts

15 January 2025When I first got a job with a 401(k) plan, I googled around to try to figure out how it worked, and everything I read went in one ear and out the other: I couldn’t keep track of how IRAs and Roths and this tax and that tax fit together. This is the guide I wish I’d had.

N.B.: I am not a tax professional, just a guy with a 401(k).

What is a retirement account?

The simplest way to save for retirement would be to stuff cash under your mattress. But money, just like a house or a car or a factory, is better used than left idle. As long as you're not using your money, you can let someone else use it, and get paid for doing so. The easiest way to lend out your money is to buy stocks and bonds.

To do so, you'll need a brokerage account, which is like a bank account except that besides dollars, it can also hold stocks, bonds, and other investments. You might open one through a company like Vanguard, Charles Schwab, or (if you were born holding a smartphone) Robinhood.

A retirement account is a brokerage account that the IRS has stamped with a fancy stamp that says “if you use this, special tax rules apply to you.” Usually those rules mean you get to pay less tax.

Why do retirement accounts exist?

The idea is that when people save for retirement, that’s good for society—it makes them more likely to stay independent and less likely to depend on welfare. So we incentivize people to save by offering them tax breaks.

If retirement accounts are so great, why do people ever use non-retirement accounts?

Retirement accounts typically have three disadvantages.

First, you can only put in money you earn yourself, as a wage or through self-employment, and only in the year you earn it (or sometimes soon after). If you receive money as a gift, for instance, you can’t put it in a retirement account.

(No one’s tracking which dollar bills end up where, so in effect, this just means that over the course of the year, the total amount you contribute to all your retirement accounts can’t be more than the amount you earned.)

Second, there’s a limit on how much you can put in each year. Many people hit the limit and put the rest of their savings into a regular brokerage account.

Third, you aren’t supposed to take your money out until you reach retirement age, around 55–60. I say “supposed” to because often you can take it out earlier without much of a penalty, which makes retirement accounts useful for all kinds of long-term savings (think 5–10 years or longer).

Which taxes can you avoid?

Suppose you open a (non-retirement) brokerage account, deposit your paycheck, use those dollars to buy shares in an index fund, wait until you retire, and then sell those shares to withdraw your money. You’ll pay taxes twice:

- You’ll pay income tax on the money you earn in the year you earn it.

- When you sell your investments, if they’ve increased in value, you’ll pay capital gains tax on that increase.[^1]

Retirement accounts let you avoid one or both of these taxes.

How much money can retirement accounts earn you?

Or, are retirement accounts worth your precious attention?

Hardly anyone even tries to answer this question. I assume they’re scared off by the sensitivity of the answer to a host of personal factors. But a ballpark number is better than no number, and I am determined to give you one.

The only analysis I could find, from Aaron Brask, says the benefits of retirement accounts are an extra 0.7% to 2.7% in returns each year. Over 10 years, that’d be a 5%–30% total gain; over 25 years, a 20–90% gain.[^2]

My own rough calculation suggested that for a young person holding index funds, using a retirement account will mean between 10% and 30% more money available to spend in retirement, as compared to making the same investments in a non-retirement account. I don’t have those notes anymore, so I’m not sure how to square them with Brask’s numbers.

Tax advantages: Roth vs. traditional

There are two main types of retirement accounts, traditional and Roth, providing different tax advantages.

The advantage of a Roth account is easier to understand: when you take money out of a Roth account, you get to skip the capital gains tax. We can tell right away that, if you’re going to hold your money to retirement, a Roth account is strictly better than a non-retirement account.

Traditional accounts are more complicated. When you put money in a traditional account, you typically[^3] get to skip the income tax. But instead, when you withdraw the money, there’s an upside and a downside. The upside is that you don’t have to pay capital gains tax on the earnings. The downside is that you do have to pay income tax at your current tax rate on both the principal (the amount you originally put in) and the earnings.

| Non-retirement account | Roth account | Traditional account | |

|---|---|---|---|

| Income tax when you contribute money | Yes | Yes | No |

| Capital gains tax on earnings when you withdraw money | Yes | No | No |

| Income tax on principal and earnings when you withdraw money | No | No | Yes |

| Restrictions | None | Earned income | Earned income |

Which is the better deal?

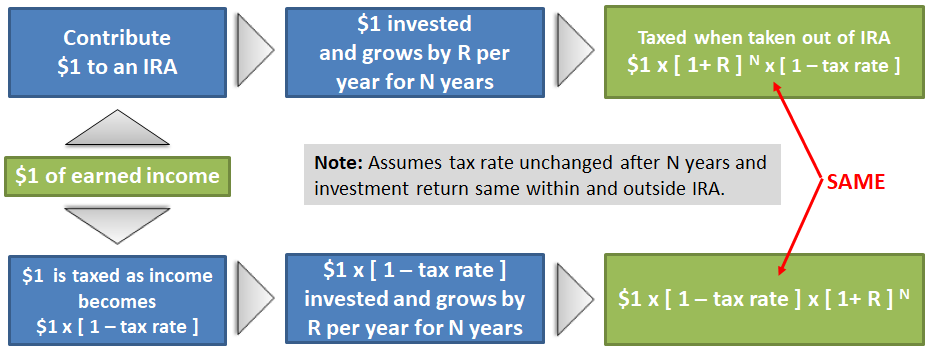

Suppose there were one constant marginal tax rate for everyone. In that case, paying income tax on principal and earnings when you withdraw is equivalent to paying income tax when you contribute. (You can see that illustrated mathematically here.) Roth and traditional accounts would be equivalent.

{kind=link}

So the question of whether to use a traditional or Roth account is a question of how your marginal tax rate will change over time. And in the U.S., income taxes are progressive: the more you earn in a year, the higher your marginal tax rate. (If you need a primer on tax brackets, try this video.)

So, to a first approximation, if you expect your income to go up, Roth accounts are better. If you expect it to go down, traditional accounts are better. (Another important factor is which state you plan to be paying taxes in.)

Note that money withdrawn from a traditional account also counts as income for the purpose of calculating your marginal tax rate.

Traditional and Roth accounts differ in other ways as well, like when you can take your money out; it’s often easier to withdraw from a Roth account. See here for a discussion of many more factors.

How do you actually cash in on a tax break?

If you have a traditional account, you’ll get to “skip” income tax by deducting contributions on your income taxes in the year you contribute. And for either kind of account, you’ll get to “skip” capital gains tax by… not reporting any capital gains. (Though depending on what kind of account you have, you might have to submit some forms about your account anyway; your account provider will send them to you and you’ll upload them into your tax software and it will take care of things.)

401(k)s and IRAs

We unfortunately need to discuss a dull technicality concerning the two main ways you can set up a retirement account.

Some accounts any individual can open for themselves; the most common one is the Individual Retirement Account (IRA). Other accounts are managed by employers on behalf of their employees; the most important of these is the 401(k), named memorably after section 401(k) of the Internal Revenue Code.

Why two different types of accounts? Why not get rid of accounts tied to employers and save some neurons in everyone’s brains? Plausibly because more people are willing to opt in to automatic 401(k) allocations than will go and deposit money into their IRAs.

Each type of account has a Roth and traditional variant:

| Pay income tax later | Pay income tax now | |

|---|---|---|

| Employer-managed | (Traditional) 401(k) | Roth 401(k) |

| Individually-managed | (Traditional) IRA | Roth IRA |

One advantage of a 401(k) is that many employers have matching programs, where they will contribute $1 for every $1 you contribute, up to a limit. (This matching contribution will always go to a traditional account.) That’s free money.

The next sections will look at how IRAs and 401(k)s stack up against each other along different dimensions, starting with…

Contribution limits

The IRS limits your total contribution to all IRAs to ~$6k in 2023. In addition, if your income is more than ~$83k and you have access to a 401(k) through your employer, there are special rules that will prevent you from getting any tax benefits unless you use the somewhat-less-convenient backdoor Roth IRA trick.

For 401(k)s, the IRS limits your total contribution to ~$20k, although there are loopholes that let you get up to ~$60k (as of 2023).[^4]

Withdrawal restrictions

You can withdraw the amount you put into a Roth IRA—though not the earnings—whenever you want, penalty- and tax-free.

You can do the same for a Roth 401(k), though with some extra wrinkles.[^5] There are also many extenuating circumstances in which you can withdraw earnings from a 401(k) without penalties: for instance, you can withdraw without penalty to pay for medical bills or college tuition, to avoid losing your home, or if you set up a fixed schedule of withdrawals over several years.

Traditional accounts have more restrictions around withdrawals. Before retirement age, you’ll typically be penalized if you withdraw; after retirement age, you’ll typically be required to withdraw certain amounts each year. These “required minimum distributions” can lump your income into a few years, which—because of the progressive tax rate—means you pay more total tax.

If you’re going to keep big sums in traditional accounts, be aware of these restrictions.

Backdoors

“Backdoors” are strategies for moving money between accounts. They’re called backdoors because the writers of the tax code didn’t foresee them. They’re perfectly legal.

The “backdoor Roth IRA” lets you get around the IRA contribution limit, letting you contribute to an IRA when your income would otherwise make you ineligible.

The “mega backdoor Roth 401(k)” lets you get around the 401(k) contribution limit, doubling or tripling the total amount of money you’re putting into retirement accounts.

These aren’t particularly difficult to set up, but you will want to read the fine print on these, because (like everything else) they have some quirks.

Final thoughts

My conclusion: if you’ve got money you plan to save for at least five or ten years, put it into retirement accounts.

Roth accounts can rarely hurt: if you need the money before retirement, you’ll be able to get most of it out without penalties; in the worst case, you’ll have to pay the taxes you would’ve otherwise paid plus a 10% penalty.

Traditional accounts can be an even better deal if you earn a lot of money and are pretty sure you won’t need it before retirement.

Whether you contribute to a 401(k) or an IRA doesn’t matter much. But if your employer offers matching 401(k) contributions, make sure to use them.

For up-to-date contribution limits and restrictions, Nerdwallet seems to have pretty good articles. For a plug-and-play strategy, maybe try this flowchart.

{kind=link}

A few final thoughts:

- Don’t forget to donate to charity—it’s tax-deductible!

- Although IRAs and 401(k)s are the most widely useful retirement accounts, there are others, notably the Health Savings Account (HSA).

- Consider spending money. Saving isn’t always prudent.

[^1]: You’ll also pay capital gains tax if you change which investments you’re holding—for instance, if you sell MSFT to buy APPL, or sell APPL to buy treasury bonds. But most people should never need to do this: just buy a retirement target fund and hold it. [^2]: That’s assuming you rebalance your portfolio every year, which index fund holders won’t need to do; so the true benefits might be even greater. [^3]: You can also contribute to a traditional account “after-tax,” meaning you pay taxes when you contribute and when you withdraw. It’s just as bad a deal as it sounds—unless you use a backdoor, a loophole that allows you to move your money into a Roth account, in which case it can become a very good deal. [^4]: Technically, you can still contribute “after-tax”. As mentioned above, this is a bad idea unless you’re using a backdoor. [^5]: For instance, you may need to move the money into a Roth IRA that has been open for five years—even if it’s sitting empty—in order to do this. More info.